WASHINGTON — The Supreme Court heard oral arguments in Consumer Finance Protection Bureau (CFPB) v. Community Financial Services Agency of America (CFSA) on Tuesday, in a crucial case at the crossroads of Congress’s ability to fund government agencies and the interests of consumer protection.

The central issue is whether the CFPB’s regulations are invalid because the bureau receives its budget from the Federal Reserve and not directly through Congress. The CFSA, an association representing payday lenders, argues that the CFPB’s funding insulates it from checks and balances and grants it excessive power, while proponents of the CFPB including the Biden administration contend that its separation from the partisan world of politics keeps the agency running effectively.

The CFPB argued on Tuesday that there is a strong historical precedent for government agencies to be funded in the same way as the CFPB is. Elizabeth Prelogar, U.S. solicitor general, cited the Customs Service, the Post Office and the National Mint as examples of agencies given significant discretion over their spending.

Chief Justice John G. Roberts Jr. asserted that the petitioners took an aggressive view of Congress’s authority under the appropriations clause, but he stressed that he did not disagree with the stance. He raised the concern that if the same political party controlled the executive and legislative branches, ruling in favor of the CFPB could give them powers not intended by the framers of the Constitution.

“If you look at it through that lens, then history should play a powerful role in trying to understand the limits or scope of how much Congress can give away,” Prelogar said. “Here, the court doesn’t need to articulate any outer limit because we have a specific type of appropriation that is far more constrained.”

The Dodd-Frank Act created the Consumer Protection Financial Bureau after the financial crisis in 2008. Congress passed the legislation to prevent catastrophic recessions caused by fraud from recurring.

“In its 12-year history, the agency has returned a whopping $17.5 billion to exploited consumers,” Patrick Gaspard, president of the Center for American Progress, said in a panel last week. “Its mission is explicitly non-political, and pretty darn straightforward: Protect everyday Americans from getting hosed.”

The CFPB makes rules for banks and other financial institutions, seeking to protect consumers from deceptive and predatory loans. These rules cover credit card payments, student loans, among other financial issues.

Sen. Elizabeth Warren (D-Mass.), who strongly advocated for and helped create the CFPB, said all financial regulators – such as the Federal Reserve, the FDIC and the CFPB – are designed to function all the time regardless of the political state of the country.

“Starting back in 1863, with our very first banking regulator, Congress decided to protect the integrity of these regulators from the chaos and the politicking of the annual appropriations process by giving them independent funding structures,” Warren said at the panel last week. “There is no constitutional basis for requiring Congress to do otherwise.”

The main question before the Supreme Court is whether whether CFPB’s funding violates the appropriations clause of the Constitution. Former Justice George Sutherland, who was on the high court from 1922-1938, said the appropriations clause prevents money from being paid out of the Treasury “unless it has been appropriated by an act of Congress.”

The CFPB receives its funding from the Federal Reserve rather than the U.S. Treasury. The U.S. Treasury is a government entity responsible for enacting fiscal policy like collecting taxes and managing the national debt. Congress usually takes money from the Treasury, which is partially funded by citizen tax dollars, to fund its projects and agencies.

The Federal Reserve – an entity tasked with enacting monetary policy like setting interest rates and promoting economic stability – is an independent agency, though even it says that it is “one that is ultimately accountable to the public and the Congress.” Its funding does not come from Congress, but rather primarily from interest it earns from government securities it acquires on the open market.

It does operate under some governmental oversight as the appointment process for its key positions involves both the executive and legislative branches.

During oral arguments, the CFSA’s attorney repeatedly said the CFPB’s budget limit was “a cap so high it is almost never relevant.” This was to make the point that the CFPB currently has too much financial freedom with not enough congressional oversight.

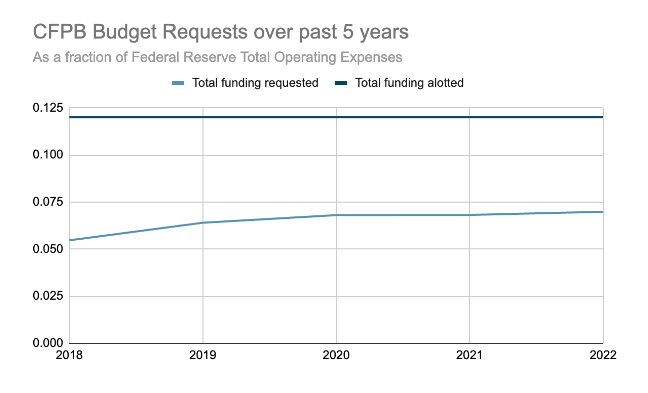

The director of the CFPB, who is nominated by the president and confirmed by the Senate, requests a percentage of their budget to be taken directly from the Federal Reserve yearly. In reality, as long as this request is less than 12% of the reserve’s total operating expenses, this request is routinely approved.

The CFPB has requested less than $650 million and less than 7% of the Federal Reserve’s total operating expenses consistently over the last five years, including in 2020 when the U.S. was facing the pandemic-induced recession.

(Matthew Vega/MNS)

Shiela Bair, the former head of the Federal Deposit Insurance Corporation, said in an article that the case could have much larger implications due to the CFPB’s nonunique funding structure. Social Security, Medicare and the Federal Reserve itself are all agencies not funded directly through Congress. Bair said these agencies could also be called into question should the court side with the CFSA.

The CFSA argued that the CFPB’s funding structure bypasses the necessary checks and balances required of government agencies and that its regulations must thus be void.

Rep. Scott Fitzgerald (R-Wis.) is urging that the CFPB’s structure should be changed so that it is funded directly through Congress to promote the principles of transparency that it preaches.

“The CFPB’s funding structure as it stands completely undermines the separation of powers and allows the agency to function as a quasi-legislative body without direct accountability to the people’s house,” Fitzgerald said in a statement.

When Justice Ketanji Brown Jackson pressed the CFSA’s attorney Noel Francisco for a constitutional basis for his argument that the structure violates the appropriations clause, Francisco pivoted instead back to the ideas of the founders that the sword and purse must be separated.

Francisco called Jackson’s understanding of the Constitution into question after she stated that the Constitution does not prohibit Congress from allowing agencies to set their own budgets within a certain requirement, Francisco said, “If that’s your position, I don’t think I can get your vote.”

The Supreme Court currently has a 6-3 conservative majority. In previous cases, such as Selia Law v. CFPB, the conservative members of the court sided against the CFPB. In that case, the Supreme Court ruled that having the director of the CFPB removable only by cause violates the separation of powers, but the bureau was still allowed to operate if a new president is allowed to change directors, which the agency did.

The Supreme Court does not set a timeline for when its decisions are released, so its opinion in this case could come as late as the end of its term in June 2024.